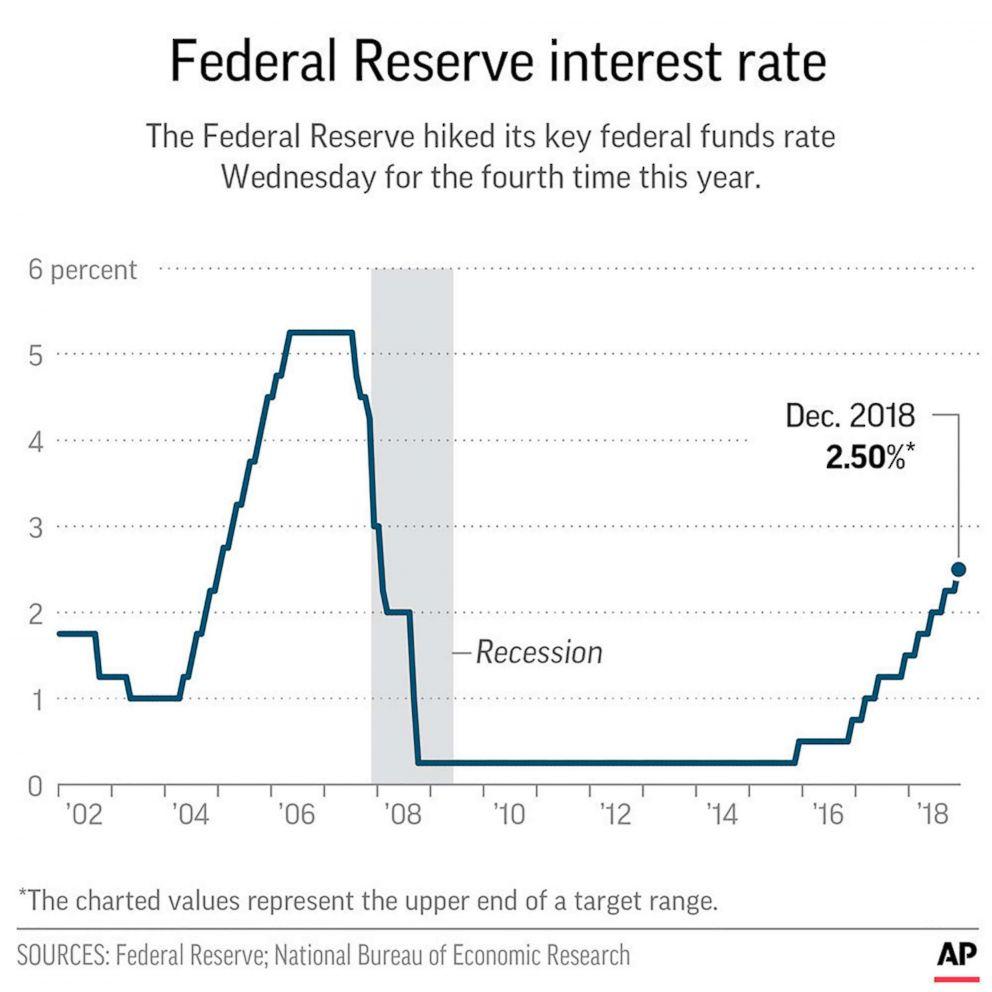

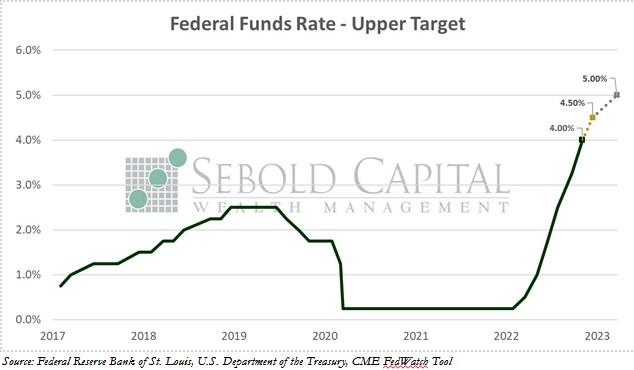

In the high-stakes financial theater, where economic decisions ripple across millions of bank accounts and investment portfolios, the Federal Reserve’s latest rate decision emerges as a pivotal performance. Like a maestro conducting a complex economic symphony, the Fed’s moves can transform the landscape of personal finance in an instant. Whether you’re a cautious saver, an aspiring homeowner, a credit card holder, or an investment strategist, understanding these monetary shifts could mean the difference between financial harmony and fiscal dissonance. This article dissects the intricate ways the Fed’s rate decision impacts your financial ecosystem, offering a clear, unvarnished view of how these seemingly abstract numbers translate into very real dollars and cents. The recent Federal Reserve’s interest rate decision sends ripples through the financial ecosystem, touching nearly every aspect of personal and household economics. When the central bank adjusts its benchmark rate, consumers experience immediate and long-lasting impacts across multiple financial instruments.

Savings accounts become more attractive during rate hikes, with customary banks gradually increasing annual percentage yields. High-yield online banks typically respond faster, offering more competitive returns that can definitely help savers grow their emergency funds and short-term reserves more effectively.

Mortgage rates experience direct correlation with Fed decisions. Fixed-rate mortgages follow long-term Treasury yields, while adjustable-rate mortgages respond more immediately. Potential homebuyers might see increased borrowing costs, possibly cooling down the real estate market and affecting property valuation strategies.

Credit card holders face the most immediate consequences. Variable interest rates tied to the prime rate mean higher monthly payments and increased overall debt burden.The average credit card annual percentage rate could jump significantly, making revolving balances more expensive and challenging to manage.

Personal loan dynamics also shift dramatically. Borrowers seeking new financing might encounter higher initial interest rates, making debt consolidation and large purchases more costly. Existing fixed-rate loans remain unaffected, providing some stability for current loan holders.

Investment portfolios experience nuanced transformations. Stock markets often react sensitively to rate changes,with growth stocks potentially experiencing more volatility. Bond markets become notably interesting, as higher rates can create opportunities for fixed-income investors seeking better yields.

Retirement accounts and 401(k) plans might see short-term fluctuations but typically demonstrate resilience. Diversified portfolios can weather rate changes more effectively,emphasizing the importance of balanced investment strategies.

Auto loans represent another critical area of impact. Financing for new and used vehicles could become more expensive, potentially influencing consumer purchasing decisions and automotive market dynamics.Buyers might need to negotiate more aggressively or consider alternative financing options.Small business owners should pay close attention to these rate adjustments. Borrowing costs for operational expenses and expansion plans could increase, requiring more strategic financial planning and potentially slowing growth initiatives.

Consumer behavior inevitably adapts to these financial shifts. Individuals might prioritize debt reduction, increase savings rates, or restructure investment portfolios to optimize their financial positions in a changing economic landscape.

Understanding these interconnected effects helps consumers make informed financial decisions, navigate economic uncertainties, and develop robust personal finance strategies tailored to evolving market conditions.